Image

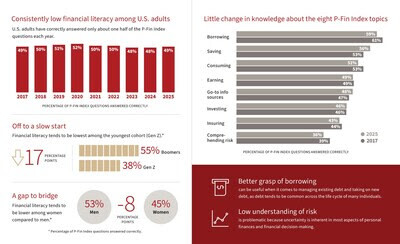

New York - May 29th - The 9th annual nation-wide Personal Finance Index (P-Fin Index) shows financial literacy remains at low levels with US adults, on average, correctly answering only 49% of the index questions across eight key personal finance areas, the same as in 2017.

The report uses 28 questions to assess financial literacy and is a joint initiative by the TIAA Institute and the Global Financial Literacy Excellence Center (GFLEC), part of the Stanford Initiative for Financial Decision-Making (IFDM). It also highlights the important role financial literacy plays in financial well-being as adults with very low financial literacy are twice as likely to be debt-constrained and three times more likely to be financially fragile compared to those with very high financial literacy.

"The persistent low levels of financial literacy underscore the need for targeted educational initiatives," said Annamaria Lusardi, an economist from Stanford University, the faculty director of IFDM, and a TIAA Institute Fellow. "To promote long-term financial security, it is essential to develop educational programs tailored to the diverse needs of various demographic groups and provide support where possible to help individuals make informed financial decisions."

Generational Differences

In addition to highlighting overall low financial literacy, the year's results reveal noteworthy differences across generations, underscoring the challenges faced by younger and older adults.

Taken together, these findings highlight a need for generationally tailored financial education: helping Gen Z establish foundational skills early and refining other generations' understanding of basic financial knowledge to help with long-term planning.

"Our research consistently shows that stronger financial literacy correlates directly with better financial outcomes – from reduced debt burdens to greater financial resilience," said David Nason, CEO of TIAA Wealth Management & Advice Solutions. "We have both an opportunity and an obligation to bridge this knowledge divide by championing financial education and delivering personalized financial guidance that resonates with everyone's unique needs and challenges. By doing so, we can empower every American to build a secure financial future and create a more inclusive financial system for all."

This year's P-Fin Index is being released to coincide with a discussion on "Measuring the Effectiveness of Financial Literacy Programs" at the U.S. Department of Treasury's public meeting of the Financial Literacy and Education Commission (FLEC.

The P-Fin Index uniquely measures both overall financial literacy and functional knowledge in eight personal finance areas – such as saving, insuring, and investing – while also gauging financial wellness and basic retirement fluency.

For more information about the 2025 P-Fin Index, see "Financial literacy and retirement fluency in America" report.

About GFLEC and IFDM

Founded in 2011 in Washington, D.C., and now housed at the Stanford Graduate School of Business, the Global Financial Literacy Excellence Center (GFLEC) is committed to advancing research and developing solutions that promote universal financial literacy. As part of Stanford University's Initiative for Financial Decision Making (IFDM), GFLEC serves as a global hub for innovative research in financial literacy and personal finance. It advances the mission of IFDM of transforming personal finance education and changing the conversation about money. For more information, visit: https://ifdm.stanford.edu/.

About TIAA Institute

The TIAA Institute* is a think-tank within TIAA, conducting cutting-edge research in the areas of financial literacy and longevity literacy, lifetime income, retirement plan design and behavioral finance in the context of retirement. The Institute provides consulting services for higher education and the broader nonprofit sector. For more information, visit www.tiaainstitute.org.

About TIAA

TIAA is a leading provider1 of secure retirements and outcome-focused investment solutions to millions of people and thousands of institutions. It shared $5 billion with participants in 2023, on top of the stated guarantees, and has $1.4 trillion in assets under management (as of 3/31/2025)2.